Many hosts are surprised to find that their most profitable-looking market can shrink significantly once taxes are factored in. Tax burdens by market reveal that cities with similar gross revenues can produce wildly different after-tax returns, flipping the ranking of what looks like a winning investment. Federal income taxes, self-employment taxes, and local occupancy levies each take a cut before you see a dollar of real profit. This guide walks through every key layer of vacation rental taxation, with concrete examples, practical rules, and clear explanations so you can make better decisions and stay fully compliant.

Table of Contents

- Tax basics every vacation rental host must know

- Schedule E vs. Schedule C: Which applies to you?

- Local occupancy taxes: What you need to collect and remit

- Maximizing deductions and avoiding costly mistakes

- How taxes really affect your rental’s profits

- The hidden costs—and opportunities—in rental tax compliance

- Take the next step to tax compliance and peace of mind

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your tax form | Short-term rental hosts must determine if they should file Schedule E or C based on activities and services offered. |

| 14-day rule benefits | Rentals of 14 days or less per year are tax-free but forfeit deductions on expenses. |

| Local taxes add up | Occupancy taxes can take a substantial bite out of profits and vary widely by market. |

| Maximize deductions | Track all allowed expenses and prorate for personal use to keep more income. |

| Compliance drives profit | Understanding and following tax rules minimizes audit risk and boosts long-term returns. |

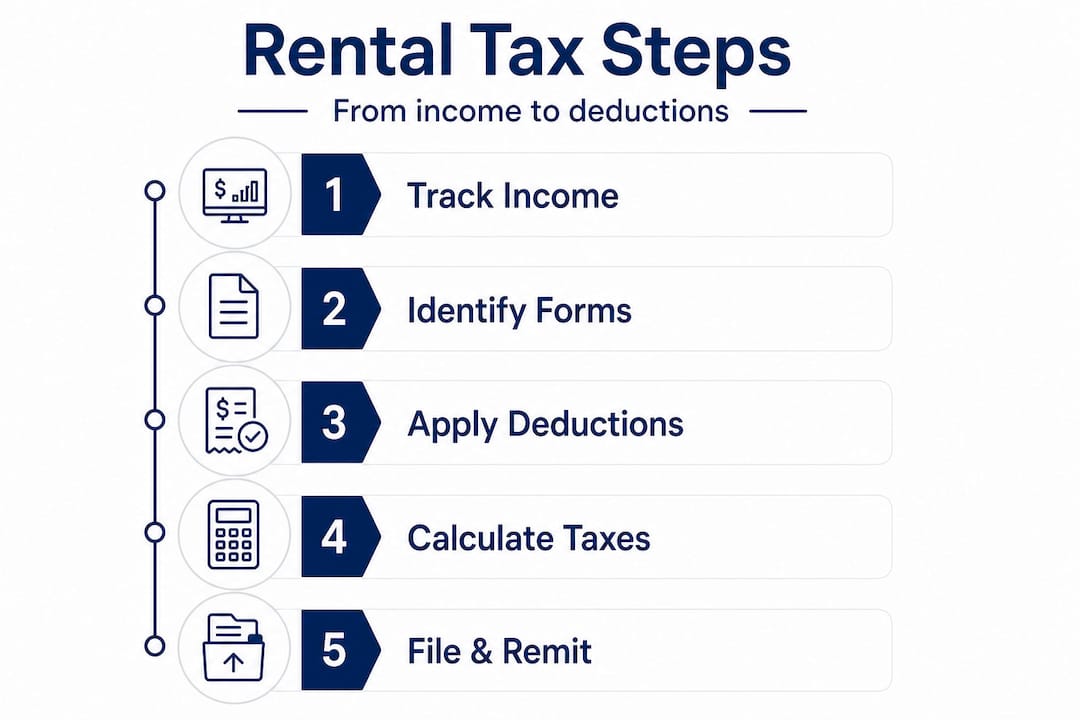

Tax basics every vacation rental host must know

Understanding what counts as taxable income is the first step toward accurate filing. Almost everything guests pay you is considered rental income, including nightly rates, cleaning fees you collect directly, and pet fees. Even small bookings you run off-platform must be reported. The IRS does not set a minimum dollar threshold before rental income becomes taxable.

You will report rental income on either Schedule E or Schedule C, depending on how you operate your rental. Schedule E is used for passive rental income, while Schedule C applies when you run your rental more like a business with substantial services. Choosing the wrong form has real consequences, from missed deductions to unnecessary self-employment taxes.

One critical rule to understand right away is the 14-day rule. The 14-day rule exempts rentals from federal income tax if you rent the property for 14 days or fewer per year, and if you personally use it for more than 14 days or 10% of the days it is rented. If both conditions are met, rental income is completely tax-free, though you cannot deduct rental expenses either. Once you exceed that threshold, all rental income becomes reportable.

Here is how tax treatment varies by rental duration:

| Days rented per year | Personal use | Tax treatment |

|---|---|---|

| 14 or fewer | Over 14 days | Income tax-free; no expense deductions |

| 15 or more | Minimal or none | Fully taxable; full deductions allowed |

| 15 or more | Over 14 days or 10% of rental days | Taxable; deductions must be prorated |

Key things to track from day one include:

- All booking payouts, including platform deposits and direct transfers

- Cleaning fees, security deposits kept, and any ancillary charges

- Your personal use days versus rented days for proration purposes

- All receipts for repairs, supplies, utilities, and platform fees

Stay current with 2026 short-term rental tax obligations to make sure you are applying the most recent IRS guidance and state-level rules.

Pro Tip: Even if a booking platform sends you a 1099-K, you are responsible for reporting all income accurately, including amounts below the 1099-K threshold. Log every payout the moment it lands.

Schedule E vs. Schedule C: Which applies to you?

With the basics set, let’s zero in on the schedules most hosts struggle with: E and C.

Schedule C applies when the average guest stay is 7 days or fewer, or when you provide substantial services similar to a hotel, such as daily cleaning, linen changes, or concierge-level assistance. Schedule E is used for longer average stays or when only standard landlord services are offered, such as providing a clean unit at the start of a stay.

Here is a side-by-side comparison:

| Factor | Schedule E | Schedule C |

|---|---|---|

| Typical use | Passive rental income | Active business income |

| Average guest stay | More than 7 days | 7 days or fewer |

| Services provided | Standard (cleaning between stays) | Substantial (daily housekeeping) |

| Self-employment tax | Not applicable | 15.3% on net profit |

| QBI deduction (20%) | Generally available | Potentially available with conditions |

| Audit risk | Lower for typical hosts | Higher without strong recordkeeping |

| Passive loss rules | Apply; losses may be limited | Losses may offset active income |

Important factors that determine your classification:

- Calculate your average guest stay length for the tax year.

- Identify every service you provide during a guest’s stay, not just before or after.

- Determine whether those services go beyond what a standard landlord offers.

- Consult the federal tax responsibilities for rentals guidelines for your specific situation.

- Make a final classification and document your reasoning before filing.

It is important to note that cleaning between guests is not considered a substantial service for Schedule C purposes. The IRS draws a clear line between services provided to maintain the property and services provided directly to guests during their stay. Daily towel changes and breakfast service push you toward Schedule C. A turnover clean between bookings does not.

If you are unsure which schedule applies, erring on the side of Schedule E is generally safer for most passive hosts. However, misclassification in either direction can trigger an audit or leave deductions on the table. A tax professional familiar with short-term rentals is worth the consultation fee.

Pro Tip: If you file under Schedule C, you owe self-employment tax (15.3%) on net profit. This can add thousands to your tax bill. However, Schedule C also allows you to deduct business-related expenses more broadly, and you may qualify for the 20% Qualified Business Income (QBI) deduction, which partially offsets that burden.

Local occupancy taxes: What you need to collect and remit

With federal rules set, you also need to know what is due locally, which can vary by city and by platform.

Local occupancy taxes go by many names: Transient Occupancy Tax (TOT), Hotel Occupancy Tax (HOT), lodging tax, and short-term rental tax. Regardless of what your jurisdiction calls it, the obligation is the same. You must either collect it from guests and remit it to the appropriate local authority, or verify that your booking platform is doing it for you. Occupancy and lodging tax rates typically range from 5% to 15%, though some markets exceed that range when state, county, and city levies are stacked.

Here is a snapshot of how taxes and collection responsibility vary by market:

| Market | Typical combined rate | Primary collector |

|---|---|---|

| San Diego, CA | 10.5% (city TOT) | Airbnb collects in most cases |

| Jackson, WY | Up to 14% combined | Depends on platform and listing type |

| Nashville, TN | 15.25% combined | Airbnb collects; others may require host remittance |

| Austin, TX | 15% combined | Airbnb collects; VRBO may split responsibility |

| Miami, FL | 13% combined | Platform or host depending on jurisdiction |

Key things to know about platform handling:

- Airbnb collects and remits TOT in many US jurisdictions automatically, but not all.

- VRBO and Booking.com may split the responsibility or leave it entirely to the host.

- Even when a platform collects taxes, the host remains legally responsible if the amount remitted is incorrect or incomplete.

- Some jurisdictions require hosts to register directly with the city tax authority regardless of what the platform handles.

For a deeper breakdown of how TOT works and where you may owe it, review the guide on understanding transient occupancy tax to check your specific market’s requirements.

Pro Tip: Never assume that because you list on a major platform, all your occupancy taxes are handled. Log into your platform’s tax settings, cross-reference your local government’s STR tax page, and verify that every applicable tax is being collected and remitted correctly.

Maximizing deductions and avoiding costly mistakes

Now that you know what you owe, let’s ensure you keep more of what you earn through smart deductions.

The IRS allows a broad range of deductions for vacation rental properties. Common deductions include mortgage interest, property taxes, insurance premiums, utilities, cleaning costs, repairs and maintenance, depreciation, and platform service fees. These deductions can significantly reduce your taxable income, but only if you document them properly and prorate them correctly when personal use is involved.

The proration rule works like this. If you rented your property for 200 days and used it personally for 50 days, then 80% of your expenses are deductible as rental expenses. The remaining 20% are personal and not deductible. This calculation applies to shared costs like utilities, mortgage interest, and insurance. Expenses that are purely rental-related, like platform fees and advertising, are 100% deductible without proration.

Deductions that hosts frequently miss include:

- Depreciation on the structure (typically over 27.5 years for residential property)

- Cost Segregation Studies that can accelerate depreciation on certain components

- Home office deduction if you manage your rental from a dedicated workspace

- Professional fees, including property managers, accountants, and attorneys

- Subscriptions for software tools used to manage your listings and compliance

- Travel expenses for property inspections or maintenance trips

Material participation can allow non-passive treatment for rental losses. This is significant because passive rental losses are normally limited to $25,000 per year and phase out entirely above $150,000 in income. If you meet the IRS material participation tests (generally, 500 or more hours of active involvement in the rental activity per year), your losses may offset other ordinary income without restriction. This can be a powerful tax planning tool for full-time hosts and active property managers.

Pro Tip: Keep a contemporaneous activity log throughout the year. Record the date, hours spent, and nature of each task you perform for your rental. This documentation is your primary defense in an audit and is essential for claiming material participation or professional real estate status.

Sloppy recordkeeping is the number one reason hosts lose deductions during an IRS examination. Receipts, bank statements, and mileage logs are not optional; they are your proof. Maintain digital backups of everything and organize them by tax year from the start.

For more details on which expenses qualify and how to apply them to deductions for short-term rentals, review the full breakdown tied to your filing classification.

How taxes really affect your rental’s profits

Finally, it’s time to see the dollar-and-cents impact, because taxes can dramatically change what a market is truly worth.

Consider two markets with similar gross revenues. On the surface, both look like strong investments. But once federal income tax, self-employment tax if applicable, and local occupancy taxes are applied, the after-tax returns can differ by thousands of dollars per year. A San Diego and Jackson WY comparison illustrates exactly this: markets with comparable gross revenue can produce very different net income once effective tax rates are applied.

Here is an illustrative example using approximate figures:

| Market | Gross annual revenue | Effective tax rate (local + federal) | Estimated after-tax net |

|---|---|---|---|

| San Diego, CA | $72,000 | 28% | $51,840 |

| Jackson, WY | $70,000 | 22% | $54,600 |

| Nashville, TN | $68,000 | 30% | $47,600 |

| Austin, TX | $65,000 | 25% | $48,750 |

Jackson, Wyoming appears to generate less gross revenue than San Diego, but its lower combined tax burden produces a higher after-tax net. Nashville generates strong gross numbers but trails all three on after-tax returns due to its combined state and city tax rate. These are real differences that change investment decisions.

Most hosts focus on occupancy rate and average daily rate when evaluating a market. Tax burden rarely makes it into the analysis until filing season arrives. At that point, the surprise is rarely a pleasant one. Factoring in the effective combined tax rate before purchasing or expanding your portfolio puts you in a stronger position to choose markets where real profit, not just gross revenue, is highest.

Building a simple after-tax cash flow model for each property takes less than an hour and can save you from investing in a market that looks great on paper but delivers disappointing net returns after every level of taxation is applied.

The hidden costs—and opportunities—in rental tax compliance

Here is a perspective that does not get enough attention in most host discussions: compliance is not just about avoiding fines. It is a growth tool.

Hosts who cut corners on tax reporting often do so thinking they are saving money. In reality, they are creating a fragile operation. Underreporting rental income or skipping occupancy tax remittance creates audit exposure that can result in back taxes, interest, and penalties that dwarf the original amount avoided. More practically, lenders and property managers increasingly ask for two to three years of clean tax returns before approving financing or partnership agreements. A host with incomplete or inconsistent filings cannot access those opportunities.

Proper compliance also creates visibility into your real numbers. When you track every dollar of income and expense accurately, you can see exactly which properties are performing and which are not. That clarity is valuable. It tells you when to reinvest, when to raise rates, and when to exit a market. Hosts who file carelessly lose that visibility along with the deductions they were entitled to.

The practical wisdom here is straightforward: document as you go, plan around after-tax cash flow, and treat compliance as an investment in the stability of your business. Review the steps outlined in legal Airbnb registration if you are still building your foundation, because tax compliance starts with proper registration, not the other way around.

Take the next step to tax compliance and peace of mind

You now have a clear picture of federal income taxes, Schedule E versus Schedule C distinctions, local occupancy tax obligations, and deduction strategies that can protect your bottom line. The next step is to verify that your specific listing is fully compliant with every layer of regulation in your market.

STR Comply makes that verification fast and free. You can check your Airbnb’s legal status in minutes, without hours of city code research or legal consultation. The platform generates a detailed, city-specific compliance summary covering permits, tax obligations, and operational restrictions. For hosts managing multiple properties, paid plans include permit tracking, renewal alerts, and ongoing regulatory updates. If you are ready to see exactly where you stand, generate a compliance report today and eliminate the guesswork before it becomes a liability.

Frequently asked questions

What tax forms do I need for Airbnb or VRBO income?

Rental hosts typically use Schedule E for passive rentals or Schedule C if providing hotel-like services. The right form depends on your average guest stay length and the level of service you provide.

Does the 14-day rule mean I never owe taxes?

Only if you rent for 14 days or fewer per year and meet the personal use threshold. The 14-day rule disallows expense deductions as well, so the exemption is a complete trade-off with no partial benefit.

How do platforms like Airbnb handle occupancy taxes?

Many platforms collect and remit state or local occupancy taxes automatically in covered jurisdictions, but hosts must verify coverage and fill any collection gaps themselves where the platform does not remit on their behalf.

Can I deduct all my expenses if I use my rental personally?

No. Proration is required when personal use exceeds 14 days or 10% of total rental days, and shared expenses must be split between personal and rental use proportionally.

What is material participation, and why does it matter?

Material participation allows you to treat rental losses as non-passive if you meet IRS activity hour thresholds, which can let those losses offset your ordinary income rather than being deferred.

Recommended

Check your city's STR regulations

Free compliance reports for 100+ US cities. Permits, taxes, zoning — all in one place.

Check My Address — Free