Many short-term rental hosts are surprised to discover that the lodging tax they owe goes by a dozen different names, follows different rules in every city, and may still require action on their part even when Airbnb or VRBO handles collection. Transient occupancy tax (TOT) is one of the most misunderstood compliance obligations in the short-term rental industry. Rates, thresholds, taxable bases, and filing deadlines all vary by jurisdiction, and getting any one of them wrong can lead to back taxes, penalties, or an audit. This article explains exactly what TOT is, how it works across different locations, what counts as taxable income, and what steps every host needs to take.

Table of Contents

- What is transient occupancy tax?

- How TOT rules differ by location

- What counts as taxable rent and fees?

- Edge cases and occupancy exceptions

- Platform collection and host compliance steps

- The hard truth: Why audits target edge-case errors

- Get compliance help and check your Airbnb legality

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| TOT applies to short stays | Most U.S. jurisdictions tax rentals of 30 days or fewer as transient occupancy. |

| Local rules vary | TOT rates, definitions, and taxable fees depend entirely on your city or county ordinance. |

| Written agreements matter | Documenting longer stays can exempt you from taxes beyond the transient threshold. |

| Platform collection isn’t enough | Hosts must still register and file even if platforms remit TOT in many cities. |

| Edge-case mistakes cause audits | Errors in stay agreements and fee bundling are a top trigger for TOT review. |

What is transient occupancy tax?

TOT is a local lodging or “hotel” tax imposed when guests occupy lodging for a short period, most commonly 30 days or fewer. Cities and counties created it to generate revenue from temporary visitors, the same way a hotel guest pays a hotel tax on checkout. Short-term rental hosts on platforms like Airbnb and VRBO fall squarely into this framework, even if the property is a private home rather than a commercial hotel.

The word “transient” is the key term here. Transient status is defined by local law based on the length of the occupancy, and jurisdictions set their own specific thresholds. In most California cities, a guest who stays fewer than 30 consecutive days is a transient. In Hawaii, the threshold is different entirely. That distinction matters enormously because a guest who crosses the threshold becomes a long-term tenant under local law, which changes the tax treatment completely.

TOT is just one name for this type of tax. You may also see it called:

- Hotel tax or hotel occupancy tax

- Transient room tax

- Lodging tax or local option lodging tax

- Tourist development tax

- Short-term rental tax

The name changes from place to place, but the underlying concept is consistent: a percentage-based tax applied to the money guests pay to stay at your property short-term. Make sure you recognize all these labels when reviewing your local ordinance, because the name on the ordinance and the name on your filing form may not match what you see in a platform’s tax center.

“TOT applies to short-term stays and is administered locally, meaning every host must verify the rules in their specific city or county, not just their state.”

How TOT rules differ by location

Now that we know what TOT is, let’s see how local rules shape what you pay and owe.

Jurisdiction matters more than anything else when calculating TOT. Two cities in the same state can have wildly different rates, thresholds, and definitions. A rate benchmarks are highly jurisdiction-specific reality means you must check the local ordinance directly rather than assuming a statewide rate applies. Solano County, California, for example, has a rate far below what Los Angeles or San Francisco charges.

Here is a quick comparison of how TOT looks across several jurisdictions:

| Jurisdiction | Tax Name | Rate (approx.) | Transient Threshold |

|---|---|---|---|

| Los Angeles, CA | Transient Occupancy Tax | 14% | Under 30 days |

| San Francisco, CA | Transient Occupancy Tax | 14% | Under 30 days |

| Solano County, CA | Transient Occupancy Tax | 5% | Under 30 days |

| Bend, OR | Room Tax | 10.4% | Under 30 days |

| Hawaii (statewide) | Transient Accommodations Tax | 10.25% | Under 180 days |

| San Diego, CA | Transient Occupancy Tax | 10.5% | Under 30 days |

Hawaii stands out immediately. While most states use a 30-day threshold to define a transient guest, Hawaii applies its Transient Accommodations Tax (TAT) to stays of fewer than 180 consecutive days. That means a guest staying for 60 or 90 days would be subject to TOT in Hawaii but might be considered a long-term tenant in California or Oregon. If you manage properties across multiple states, this kind of variation is exactly the type of detail that creates costly compliance gaps.

Beyond rates and thresholds, some jurisdictions layer additional taxes on top of the base TOT. In Hawaii, hosts pay both the TAT and the General Excise Tax, which compound the effective tax burden. In California, some cities also apply a local Measure-based surcharge on top of the base TOT rate. Staying current on those additions is part of the compliance responsibility every host carries. The STR compliance blog regularly covers changes to local ordinances as they happen, which can help you track rate updates without doing all the research yourself.

For hosts managing properties in international markets as well, a lodging tax guide comparison can offer useful context on how U.S. lodging taxes stack up against foreign equivalents, though U.S. rules remain the primary obligation for domestic operators.

What counts as taxable rent and fees?

Jurisdictional rules lead to another important question: what is actually taxed? Let’s break down the taxable base.

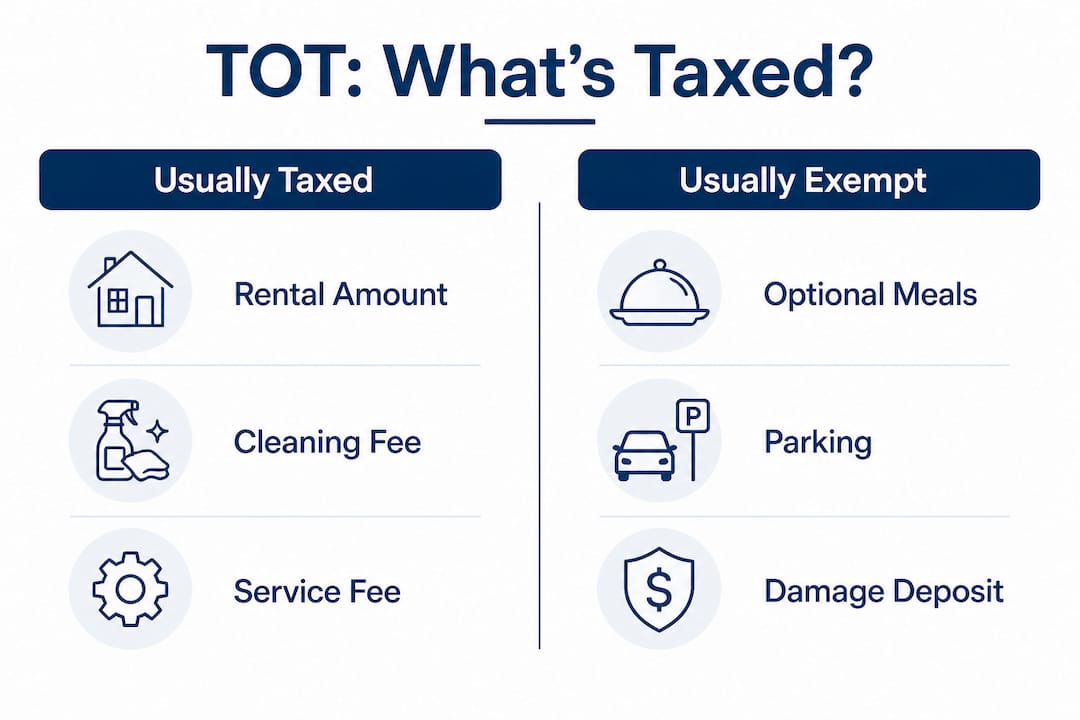

Most TOT ordinances apply the tax to “rent,” but the definition of rent is broader than many hosts expect. The taxable base varies by jurisdiction: Los Angeles treats gross rent as the basis, while San Diego defines “rent” broadly enough to capture most mandatory charges. When a guest pays your nightly rate, that amount is clearly taxable. What gets tricky is the list of fees and add-ons that surround that base rate.

Here is how common charges are typically treated:

| Fee Type | Usually Taxable | Depends on Jurisdiction | Usually Exempt |

|---|---|---|---|

| Nightly/weekly rent | Yes | ||

| Mandatory cleaning fee | Often yes | Sometimes | |

| Pet fee (mandatory) | Often yes | ||

| Optional parking | Yes | Sometimes | |

| Food and beverage service | Often exempt | ||

| Phone charges | Often exempt | ||

| Refundable security deposit | Yes (if refunded) |

The key distinction most ordinances draw is between mandatory and optional charges. If a fee is bundled into the reservation and guests cannot opt out of it, tax authorities are likely to treat it as part of the taxable rent. A cleaning fee that every guest pays, for example, is often taxable in Los Angeles even though it is listed separately from the nightly rate.

Optional charges are treated differently. If a guest can choose whether to add parking or a meal package, those charges may fall outside the taxable base depending on the local ordinance. However, do not assume an exemption applies without verifying it. Jurisdictions differ on what “optional” means, and some have updated their ordinances to capture fees that were previously excluded.

Pro Tip: Review your listing’s fee structure against your local ordinance annually. If you have added new fees since you last checked your tax obligations, you may be under-collecting and building up a liability without realizing it.

Understanding the precise TOT compliance terms used in your jurisdiction will help you map each fee in your listing to the correct tax treatment and avoid under-remitting.

Edge cases and occupancy exceptions

Understanding taxable rent is key, but hosts must also watch for occupancy edge cases that could trigger unexpected TOT liability.

Not every stay fits neatly into the “taxable” or “exempt” categories. Several edge-case scenarios create genuine compliance risk, and tax authorities know exactly where to look for them. The edge-case lens for TOT liability includes written agreements, partial days, and stays that cross the transient threshold in ways that are easy to mismanage.

Here are the most common edge cases every host should understand:

-

Threshold crossing. A guest books a 28-day stay and then extends by a week. The first 28 days were clearly subject to TOT. What about the extension? In most jurisdictions, once a stay exceeds the threshold, the guest may no longer be considered transient, but only if the proper documentation exists from the start.

-

Partial days counted as full days. If a guest checks in on a Monday evening and checks out Tuesday morning, most jurisdictions count that as one full taxable day. Never assume a partial day is exempt.

-

Written agreements for long-term exemption. Many jurisdictions allow TOT to stop accruing after the threshold date if there is a written rental agreement in place from the beginning of the stay. Without that documentation, the first 30 days may be fully taxable even if the guest stays for months. Always execute a written agreement when a guest intends to stay beyond the threshold.

-

First 30 days taxable absent proper documentation. Even in a stay that eventually qualifies as long-term, the initial transient period is still taxable. Some hosts incorrectly assume an extended stay means no TOT applies at all, which is incorrect in most jurisdictions.

-

Occupancy by employees or corporate guests. Some ordinances exempt certain corporate housing arrangements, but the exemption usually requires specific documentation such as a written corporate housing agreement. Assuming the exemption applies without paperwork is a common and costly mistake.

Pro Tip: Keep a copy of every written rental agreement, including any stay extensions. If you are ever audited, documentation of stay length and agreement terms is the first thing an auditor will request.

For hosts navigating rental agreements that push against occupancy boundaries, reviewing an Airbnb legal report for your market can clarify how local authorities interpret these edge cases. Understanding the broader context of edge-case rental laws in other markets can also offer a useful perspective on how documentation requirements function globally.

Platform collection and host compliance steps

Once you have navigated tricky occupancy cases, it is vital to understand your responsibilities around collection and compliance, even when platforms are involved.

A common misconception among hosts is that if Airbnb or VRBO collects TOT on their behalf, there is nothing left to do. That is not accurate. Platform involvement does not eliminate host compliance: hosts may need to register with the local tax authority, file periodic returns, or reconcile reported amounts even when the platform handles the actual remittance.

Here is what full compliance typically looks like for a short-term rental host:

- Register with the local tax authority. Most jurisdictions require hosts to register for a TOT account before they begin renting, not after they earn their first dollar.

- Collect the correct tax amount. Even if your platform handles collection, you need to verify the rate being applied matches the current local rate.

- Keep accurate records. Maintain records of all reservations, gross rents, fees collected, and any applicable exemptions. Most jurisdictions require records to be kept for three to five years.

- File returns on time. Compliance means registering, collecting, recording, and filing/remitting by the deadlines your jurisdiction sets. Those deadlines may be monthly, quarterly, or annual depending on your volume of activity.

- Reconcile platform collections. If a platform collects on your behalf, you may still need to report total gross receipts and reconcile them against what the platform remitted. A discrepancy can trigger a notice or an audit.

Pro Tip: Do not wait until tax filing season to check whether your platform is remitting correctly. Log into your platform’s tax summary at least quarterly and compare the amounts against your own records. Platforms occasionally miscategorize fees or fail to remit for certain markets.

The STR compliance tips available on the STR Comply blog cover platform-specific collection rules by market, which is useful when you operate across multiple jurisdictions. Keeping your short-term rental compliance obligations organized in one place significantly reduces the risk of missing a filing deadline.

The hard truth: Why audits target edge-case errors

After outlining your duties, let’s discuss why authorities focus so intently on edge cases and how to avoid the most common pitfalls.

Tax auditors reviewing short-term rental operators are not primarily interested in whether you paid a few dollars less than you owed on a straightforward nightly booking. They focus on edge cases around occupancy and bundled fees because those are the areas where systematic errors accumulate. A host who consistently fails to tax a mandatory cleaning fee, for example, may have under-remitted thousands of dollars over several years without realizing it.

Written agreements are another audit trigger. Auditors know that hosts sometimes claim long-term exemptions for guests without having the paperwork to support it. When the documentation is missing, the jurisdiction defaults to treating the entire stay as taxable, and the host owes back taxes plus interest and potentially penalties.

The most practical lesson from watching compliance cases across multiple markets is this: the hosts who face the largest assessments are not the ones who made big, obvious mistakes. They are the ones who made small, repeatable errors in gray areas, specifically around stay length documentation, mandatory fee categorization, and registration timing.

Our strong recommendation is to review your local TOT ordinance at least once a year, cross-reference your fee structure against the taxable base definition, and maintain a complete paper trail for every stay that approaches or exceeds the transient threshold. The audit compliance lessons shared through real-world cases highlight how preventable most assessments truly are. Getting ahead of the gray areas is always less expensive than resolving them after an audit letter arrives.

Get compliance help and check your Airbnb legality

As TOT enforcement gets sharper, having a compliance ally is increasingly valuable.

STR Comply is built specifically for hosts and property managers who need to stay on top of obligations like TOT without spending hours on local government websites. Whether you manage one listing or a portfolio of properties across multiple states, compliance requirements are too specific and too frequently updated to track manually.

Use the Airbnb legality check tool to instantly verify whether your listing meets local permit, tax, and zoning requirements. For a detailed breakdown of TOT obligations and edge-case guidance specific to your market, the compliance report tool delivers a city-specific summary that covers exactly what you need to know before your next filing deadline. STR Comply reduces the research burden so you can focus on running a successful rental business with confidence.

Frequently asked questions

How do I know if my rental is subject to transient occupancy tax?

Check your city or county’s definition of “transient.” Most jurisdictions apply TOT to stays under 30 days, but Hawaii uses a different threshold of 180 days, so always verify locally.

Does Airbnb or other platforms always handle TOT?

Not always. Platform involvement does not remove all host obligations; you may still need to register, file returns, or reconcile reported amounts with your local tax authority.

Which fees and charges are included in TOT?

Mandatory rent and bundled fees are usually taxable, but optional items like food service or parking may be excluded. San Diego defines rent broadly, capturing many fees that hosts assume are exempt.

What paperwork or registration is required for hosts?

Hosts typically must register for a TOT account, post a certificate, keep reservation records, and file/remit by set deadlines, whether those deadlines are monthly, quarterly, or annual.

What happens if I miss a deadline or get audited?

Late remittance and fee classification errors can trigger penalties and interest. Edge cases around occupancy and bundled fees are among the most common audit targets, making accurate documentation essential.

Recommended

Check your city's STR regulations

Free compliance reports for 100+ US cities. Permits, taxes, zoning — all in one place.

Check My Address — Free