Tax filing for vacation rentals trips up more hosts than you might expect. The IRS applies different rules depending on how many days you rent, what services you provide, and how much you earn. On top of federal requirements, local occupancy taxes and permit obligations vary city by city. Miss a form, miscalculate your rental days, or skip a W-9, and you could face withheld income, IRS scrutiny, or local fines. This guide walks you through income reporting rules, filing preparation, step-by-step instructions, and how to avoid the most costly mistakes hosts make.

Table of Contents

- Key Takeaways

- Tax filing for vacation rentals: income reporting rules

- Preparing your documents before you file

- How to file vacation rental taxes step by step

- Common pitfalls and how to handle them

- My honest take on vacation rental tax compliance

- How Strcomply helps you stay compliant

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| 14-day rule matters | Renting 14 days or fewer may exempt your rental income from federal reporting entirely. |

| Schedule C vs. Schedule E | Your service level determines which form you file, and Schedule C triggers self-employment tax. |

| W-9 is non-negotiable | Failing to submit a W-9 to your platform causes automatic 28% withholding on your payments. |

| Local taxes are separate | Occupancy and lodging taxes are a distinct obligation from your federal income tax filing. |

| Quarterly payments prevent penalties | If your expected tax liability exceeds $1,000, you must pay estimated taxes quarterly. |

Tax filing for vacation rentals: income reporting rules

The first decision you need to make is whether your rental income is reportable at all. Under the IRS 14-day rule, if you rent your property for 14 days or fewer per year and personally use it more than 14 days (or 10% of rental days, whichever is greater), that income is completely tax-free and does not need to appear on your return. It is a narrow exemption, but a real one.

Once you cross the 15-day threshold, all rental income must be reported regardless of whether a 1099-K was issued. Platforms report gross amounts to the IRS, which currently includes cleaning fees and service fees, not just the base rental payment. Your actual taxable income will differ from the gross figure on the 1099-K, so reconciliation is a required step, not optional.

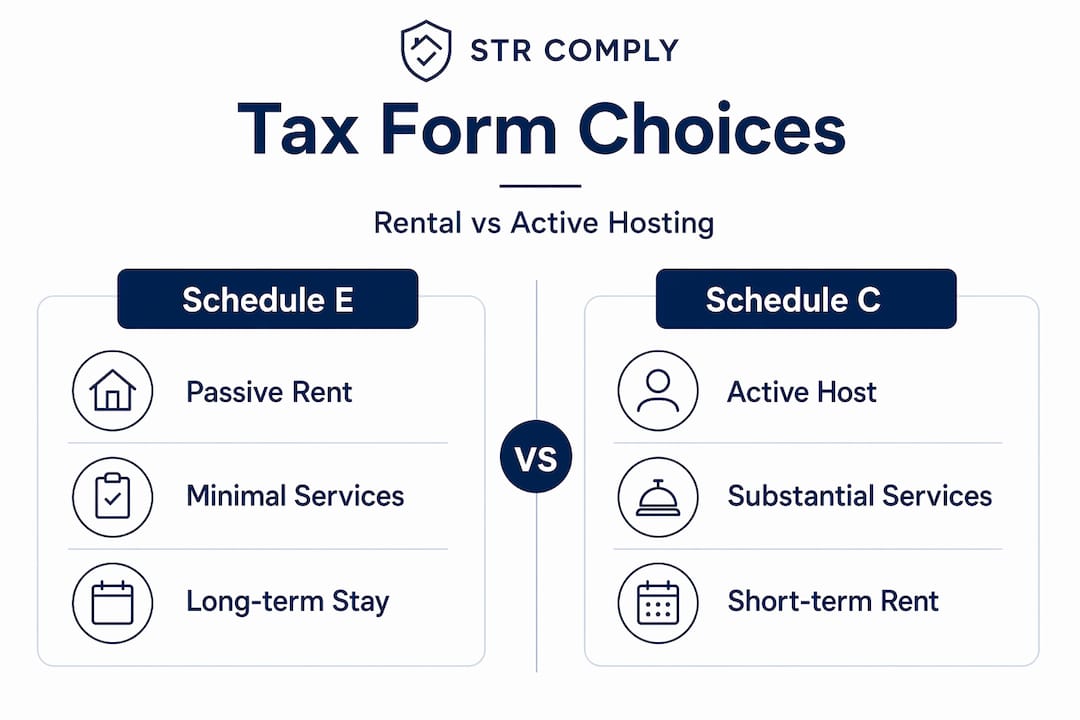

Schedule C vs. Schedule E: choosing the right form

- Schedule E applies when your rental activity is passive and you do not provide substantial services to guests. Think of it as standard landlord-style income: guests pay to stay, and you do not actively manage their experience beyond basic property use.

- Schedule C applies when you do provide substantial services, such as daily cleaning, concierge assistance, or hotel-like amenities. Schedule C income is subject to self-employment tax at 15.3%, which is a significant cost many hosts overlook.

- The line between the two is not always obvious. A host who offers weekly linen changes likely stays on Schedule E. A host offering daily breakfast and housekeeping edges toward Schedule C territory.

- Keep a log of every service you provide. This protects your position if the IRS questions your form selection.

Pro Tip: Track personal use days in a dedicated spreadsheet from day one of each calendar year. The ratio of rental days to total use days directly controls what percentage of your expenses you can deduct.

Preparing your documents before you file

Organization before filing day saves hours of work and reduces errors. Here is a practical document checklist every short-term rental host should maintain:

| Document | Purpose |

|---|---|

| Platform earnings summary | Confirms gross rental income for the year |

| Form 1099-K (if issued) | Matches IRS reporting; reconcile against actual taxable income |

| Receipts for cleaning, maintenance, and repairs | Supports deductible expense claims |

| Mortgage interest statement (Form 1098) | Prorated portion is deductible for rental days |

| Property tax records | Deductible based on rental use percentage |

| Depreciation schedule | Tracks annual deductions for property and improvements |

| Local occupancy tax filings and receipts | Documents remittance to local authorities |

Beyond gathering documents, you need to calculate the precise split between personal use days and rental days. If you used a beach house for 30 days personally and rented it 90 days, 75% of eligible expenses are deductible. That proration applies to mortgage interest, property taxes, utilities, and insurance. Get the math wrong and you are either leaving deductions on the table or overclaiming.

![]()

Local lodging and occupancy taxes are a separate layer entirely. Cities, counties, and states each set their own transient occupancy tax rates and collection deadlines. Some jurisdictions require platforms to collect and remit on your behalf. Others place that obligation directly on you. Verify your local rules before filing.

One of the most avoidable cash-flow problems new hosts face: failing to submit a W-9 to Airbnb, VRBO, or whichever platform you use. Without it, platforms are required to withhold 28% of your gross payments as backup withholding. Submit your W-9 immediately when you create a new listing.

Pro Tip: Ask your platform directly whether they remit occupancy taxes on your behalf in your specific city. The answer changes by location and year. Do not assume they do.

How to file vacation rental taxes step by step

Filing vacation rental income correctly requires a clear sequence of decisions.

-

Determine your rental day count. Count all days the property was rented to guests at fair market value. This determines whether you fall under the 14-day exemption or need to report income.

-

Select your tax form. Use Schedule E for passive rental income without substantial services. Use Schedule C if you provide significant guest-facing services. If uncertain, consult a tax professional before filing, not after.

-

Calculate your deductible expenses. Common deductible costs include cleaning fees, platform service fees, maintenance and repairs, insurance, mortgage interest, property taxes, and utilities. Each must be prorated based on your rental-day percentage if there is any personal use.

-

Account for depreciation. Residential rental property depreciates over 27.5 years. Hosts who want to accelerate deductions can commission a cost segregation study. Combined with active participation rules, this can unlock significant first-year deductions for qualifying short-term rental operators.

-

Calculate self-employment tax if on Schedule C. If you file on Schedule C, you owe self-employment tax on net earnings in addition to regular income tax. You can deduct half the SE tax from your gross income, which reduces your adjusted gross income.

-

Check for the short-term rental tax loophole. Hosts with stays averaging fewer than seven days who meet material participation standards may be able to offset ordinary income with rental losses. This requires substantial involvement and thorough documentation. It is not automatic, but it is legal and powerful.

-

File by the deadline and pay estimated taxes. The annual filing deadline is April 15. If your expected tax liability exceeds $1,000, you must make quarterly estimated payments on April 15, June 15, September 15, and January 15 of the following year to avoid underpayment penalties.

-

File local occupancy tax returns separately. Federal and state income tax filings do not cover lodging tax. Submit those returns to your city or county on the required schedule, whether monthly, quarterly, or annually.

Common pitfalls and how to handle them

Vacation rental hosts repeat certain mistakes often enough that they deserve direct attention.

- Misreporting income from a 1099-K. Entering the gross 1099-K amount as taxable income without subtracting platform fees and cleaning fees overstates your liability. Reconcile each line carefully.

- Incorrectly applying the 14-day exemption. Renting 15 days or more means every dollar is reportable. Some hosts assume occasional rentals are fine to omit. They are not.

- Mixing personal and rental expenses. Deducting 100% of a utility bill when you personally used the property for half the year is an audit flag. Prorate everything with documented day counts.

- Missing local permit requirements. Local governments increasingly require registration, inspections, and occupancy tax collection from hosts directly. Operating without a permit exposes you to fines and potential de-listing.

Short-term rental operators spend 50 to 200 hours annually on lodging tax compliance, and 44% still report feeling only somewhat confident about their compliance status.

If you receive an IRS notice related to a 1099-K discrepancy, respond promptly with documentation showing how you reconciled the gross amount to your reported income. Keep copies of your rental calendar, expense receipts, and any platform statements for at least three years after filing.

Automated tax compliance platforms and record-keeping systems reduce the time burden significantly. Reviewing your local STR tax obligations at the start of each year prevents last-minute scrambles and keeps you ahead of regulatory changes.

Pro Tip: Set a recurring calendar reminder on January 1 to pull your year-end platform summary, verify your permit renewal dates, and confirm local occupancy tax rates. Regulations shift more often than most hosts realize.

My honest take on vacation rental tax compliance

I’ve worked with enough short-term rental hosts to say this clearly: the people who struggle most with taxes are not the ones with complicated situations. They are the ones who assume their situation is simple.

A host renting a spare bedroom 60 nights a year thinks, “It’s not that much money.” But between the Schedule E vs. Schedule C question, the proration of shared household expenses, the local lodging tax filing, and the W-9 they never submitted, their “simple” situation has four potential problem areas. I’ve seen hosts receive IRS notices over income they did not even know was reportable, simply because they did not understand the 1099-K reconciliation requirement.

What actually works is treating your rental like a small business from day one. That means a dedicated folder for receipts, a rental calendar you update in real time, and a conversation with a tax professional before your first full year of operation, not the April before your deadline. Tax advisors who specialize in real estate can identify opportunities like the short-term rental tax loophole or cost segregation that generic software will miss entirely.

The compliance side, meaning permits, occupancy taxes, and registration, is equally underestimated. Nearly a quarter of hosts spend over 100 hours per year managing lodging tax compliance alone. That is not a tax problem. That is a systems problem. Hosts who invest early in structured record keeping and compliance tools consistently report less stress and better financial outcomes. Compliance does not have to be a burden. It becomes one only when it is ignored until it is urgent.

— Jure

How Strcomply helps you stay compliant

Tax obligations do not exist in isolation. Every filing decision connects to your local permit status, zoning classification, and occupancy tax registration. Strcomply gives you a fast, free way to check your listing’s compliance across all of those dimensions at once, with city-specific results in under 30 seconds.

For hosts managing multiple properties, Strcomply’s paid plans include a compliance dashboard with permit tracking, renewal alerts, and regulatory updates across markets. As a short-term rental tax compliance platform built specifically for Airbnb, VRBO, and similar listings, Strcomply removes the guesswork from both tax registration and ongoing local compliance. If you want to file with confidence and stay ahead of regulatory changes, start with a free compliance check today.

FAQ

What is the 14-day rule for vacation rental taxes?

Under IRS rules, if you rent your property for 14 days or fewer per year and personally use it more than the greater of 14 days or 10% of rental days, the rental income is tax-free and does not need to be reported. Once you rent for 15 or more days, all rental income becomes reportable.

Do I use Schedule C or Schedule E for my vacation rental?

Use Schedule E for passive rental income where you do not provide substantial guest services. Use Schedule C if you provide significant services like daily cleaning or concierge assistance. Schedule C income is also subject to self-employment tax at 15.3%, which Schedule E income is not.

What happens if I don’t submit a W-9 to Airbnb or VRBO?

Platforms are required to apply 28% backup withholding to your gross rental payments if you have not submitted a W-9. Submit the form immediately when you create or update a listing to prevent automatic deductions from your payouts.

When do I need to make estimated quarterly tax payments?

If you expect to owe more than $1,000 in federal taxes on your vacation rental income, you must make quarterly estimated payments. The payment dates are April 15, June 15, September 15, and January 15 of the following year.

Are local occupancy taxes separate from my federal tax filing?

Yes. Transient occupancy taxes and lodging taxes are collected by city and county governments and filed on a separate schedule from your federal or state income tax return. Some platforms remit these on your behalf in certain jurisdictions, but you should verify this directly for your specific location.

Recommended

Check your city's STR regulations

Free compliance reports for 100+ US cities. Permits, taxes, zoning — all in one place.

Check My Address — Free